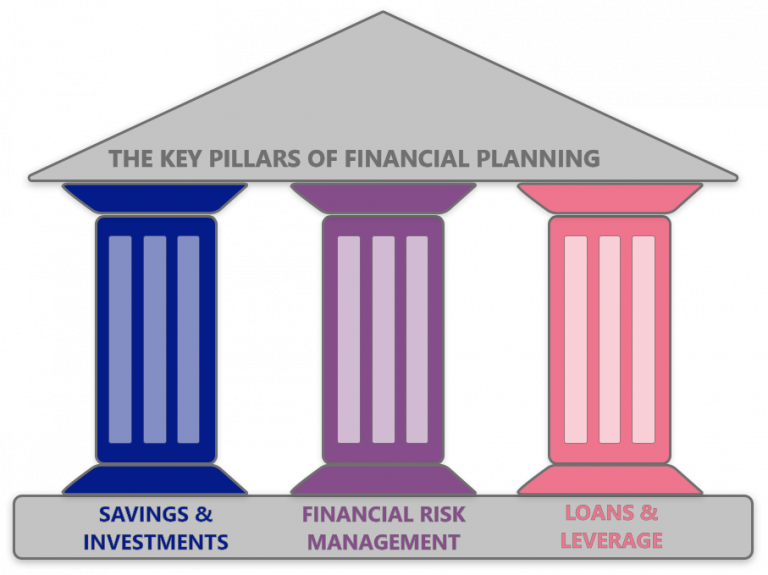

Loans often account for a considerable and often inevitable component of our liabilities, be it housing or education loan, or personal loans needed during emergencies, or loans that are inherited. They can be a saviour in times of extreme need when all else fails and can even serve as a powerful tool to grow our wealth when used wisely as leverage. On the flipside, they can be extremely detrimental when managed poorly. Therefore, a good financial plan must enable effective management of loans and leverage.