At some point of time in life, someone, somewhere has tried to sell you an insurance policy. The idea of insurance may remind you of experiences of hard-selling, pushy sales people, and incessant nudges from that annoying relative / friend, just to get you to sign up for a policy. So, why does that happen? The answer is simple – insurance needs to be “sold”. Most people do not understand the importance of insurance and will not actively seek it out. This lack of knowledge amongst the public and the insurance companies’ aggressive selling techniques has brought the insurance industry a bad reputation and has created a negative connotation for insurance itself. In this blog post, we aim to address this knowledge gap and explain why life coverage is the most important financial product you’ll ever buy.

What is life coverage?

Life insurance is a contract between an insurer and a policyholder where the insurer guarantees payment of a death benefit upon the death of the insured, in exchange of premiums paid. By setting aside less than 1% of your income, you can protect your loved ones from financial risks in the event of your passing.

Why is life coverage important?

College sweethearts Raj and Priya were ambitious young adults with big dreams. They had recently gotten married and were excited to build their life together. In an unfortunate turn of events, Priya tragically passed away from a car accident. Raj was left behind taking care of their 2 kids, paying their mortgage and study loans, and managing all their expenses with only half the household income. The sudden financial burden exhausted all their hard-earned savings within a year, putting additional strain on the family on top of the grief of losing his partner.

The above example is for a dual income family. Now imagine a situation where the sole breadwinner is not insured. Any unfortunate loss of their life could be catastrophic for the family, threatening their very survival.

Life coverage helps us prepare for such eventualities, to help mitigate the financial impact of someone’s passing. For instance, a life insurance payout would not only have helped Raj maintain his savings, but also helped to make up for the drastic dip in the household income.

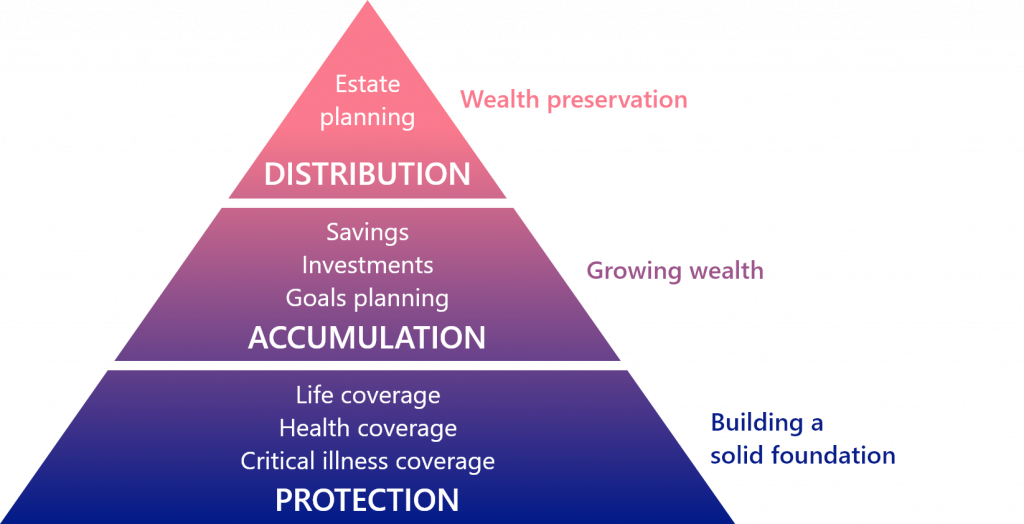

The Financial Needs Hierarchy Pyramid demonstrates the critical role of such financial protection in your overall financial planning and goals. It is important to build a solid foundation by insuring yourself for emergencies before you proceed to the higher levels of growing your wealth and building your legacy. No matter how much you save and invest, if you haven’t managed the financial risks with the appropriate insurance solutions, it could all come crashing down like a house of cards.

Financial Needs Hierarchy Pyramid

Do I need life coverage?

The answer to this question differs depending on the family and dependents’ situations. Let us analyze the possible scenarios.

- I have a family dependent on me: For those who have dependents, it is absolutely critical to get life coverage to ensure the dependents are supported after their passing. The coverage needs to factor in the number of years that we need to support our dependents. For example, kids may need to be taken care of until they graduate. As for parents and spouses, we may need to provide for their entire lifetime.

- I have a family that is not dependent on me: This might be applicable for dual income families or one with older kids. However, all of the family’s plans and dreams have been formulated with a dual income in mind. If part of this income were to stop prematurely, it would severely compromise the quality of life.

- I do not intend to have family: For the lone wolf who does not intend to have any dependents, life insurance might not be critical. However, it is a useful tool to manage one’s estate after they pass on, in case we want the transfer of our assets to certain people / organizations.

- I will have a family later: Some people may not have dependents now, but may have dependents in the future. This group still needs to get insurance as they may face hurdles due to their age or health if they leave it to later. This is explained in the next section.

When should I get life coverage?

The best time to buy life coverage is as soon as you can. There are two main reasons for this –

- Cost of insurance: Getting term insurance earlier in life saves us a lot of money in the long term. For example, a term plan purchased in the 20s, costs a fraction of what it would cost in the 40s. The difference can be as significant as 300%.

- Health: It is important to purchase life coverage when we are still healthy. If we try to delay the purchase, it might cost us more by virtue of health conditions. In fact, we might become uninsurable for certain health conditions and might not be able to get coverage at all.

Benefits beyond insurance payout amount

Estate management: This is where life insurance means much more than it’s monetary value by providing peace of mind to the insured. If someone were to pass on without life coverage, their assets would need to be immediately liquidated and distributed among the family. This process can take several years, subject to administrative hassle and family disputes, not to mention the market fluctuation in case of investment liquidation. Life coverage provides immediate liquidity to the family proportionately, so that emergency liquidation of assets is not needed and the current lifestyle does not need to be downgraded.

The Bottom Line

Effective financial risk management forms the foundation for a good financial plan. Insurance ensures that your finances are protected from the uncertainties of life so that you can focus on growing your wealth and achieving your dreams. Imagine trying to build a mansion without flood embankments and earthquake protection. Your dream could be taken away from you by one unfortunate event. Life coverage acts as this flood embankment or earthquake protection for your life.

It is important that you choose the right kind of life coverage that best meets your needs. This can be challenging with the options available out there. We have simplified the choices and considerations for you in our post on Term Vs Life Insurance.