Just a few years back, India was a country with relatively affordable healthcare services. However, this perception and the cost of healthcare has changed rapidly with rising inflation in healthcare costs, which is double the average retail inflation (CPI). Now a major illness could affect your bank account significantly, depleting your hard earned savings. Just for instance, a liver transplant on average costs 25-35 lakhs in lndia today. The increasing trend in cost of treatments and medicines is expected to continue for the foreseeable future.

Yet, data from the Insurance Regulatory and Development Authority of India shows that only 44% of Indians had health insurance in 2018. Of this, only 8% are voluntary, non-government health insurance schemes. We deep dive into some of the barriers for individuals to sign up for health insurance schemes and why it is critical for everyone to have it.

Common barriers to getting health insurance

Health insurance is one of the most basic financial tools that each and every one of us must have, no exceptions. However, there are a number of barriers that have led to a less than desirable ratio of the Indian population having health insurance. Let’s look at some of the common reasons cited by people for not getting this critical coverage and why they need to change their mindset.

I don’t have money to pay for health insurance

All health insurance plans are not identical and do not cost the same. You can customise your coverage amount, hospitals covered, modify deductible amounts, etc. to change how much the plan costs such that it fits into your budget. As long as your basic needs for survival are being met, make sure you invest in a health insurance plan before putting money into your other goals. It is important to remember that by trying to save money by not getting health insurance, you are putting yourself at great risk financially should a medical emergency arise.

I have more than enough money to pay for medical emergencies

While having sufficient savings and assets does put you in a more privileged position to manage any medical needs, using your own assets as insurance for emergencies exposes your portfolio to too much risk. Risk management is one of the most important aspects of financial planning that you need to focus on to preserve your wealth. If all your assets are insured (e.g. home insurance, car insurance), why should your most critical asset, your own health, be uninsured?

I have parents or relatives to help me in case of emergencies

The same logic applies here as the previous point. Would you want to expose the assets of your loved ones to uncapped medical liabilities? A bonus point to consider – being financially independent, even during emergencies is a gratifying feeling. Imagine never having to rely on anyone for your financial needs. Sign me up!

I have health insurance coverage from my company

Having a company group insurance coverage is a great benefit to have. It helps you take care of most basic healthcare needs. However, due to coverage limits for group insurance plans, they are generally not sufficient to cover large bills often associated with critical illnesses – situations when you most need coverage. Moreover, you will need to get personal health insurance if you leave the company or retire. The concern is that if you have developed any medical conditions by then, they will probably be excluded and not be covered under your policy, leaving you stranded. Get health insurance while you’re still young and healthy!

I have health insurance for myself but not for my dependents

Have kids, spouse or ageing parents that depend on you? Make sure you either sign them up for health insurance or include them into your own plan. This is especially important for situations such as ageing parents who have a higher probability of needing medical care. Having health coverage will ensure you have peace of mind that your loved ones’ can get the necessary healthcare support if required, while simultaneously preventing any major financial repercussions for the family.

Role of health insurance in your financial planning

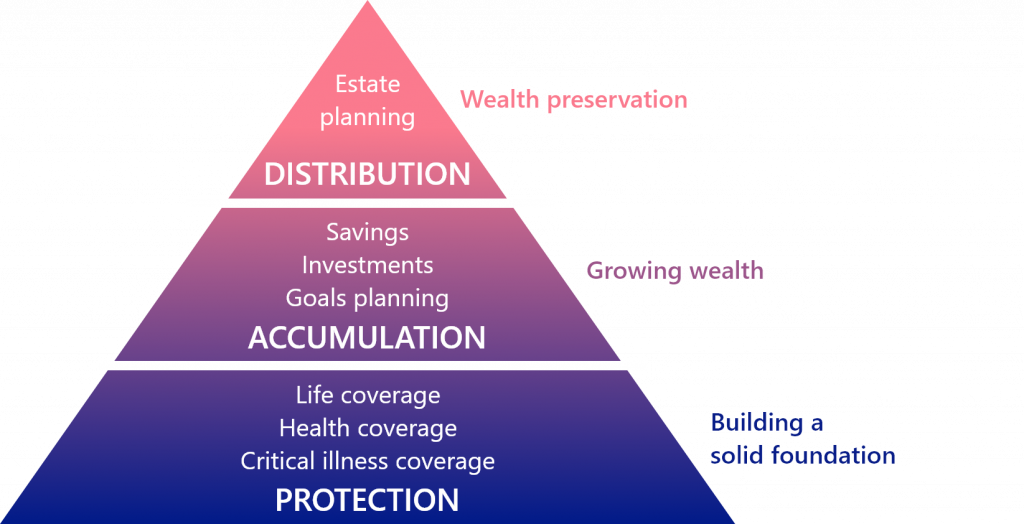

The Financial Needs Hierarchy Pyramid demonstrates the critical role of financial protection in your overall financial planning and goals. It is important to build a solid foundation by insuring yourself for emergencies before you proceed to the higher levels of growing your wealth and building your legacy. No matter how much you save and invest, if you haven’t managed the financial risks with the appropriate insurance solutions, it could all come crashing down like a house of cards. Health insurance is one of the most basic risk management tools at your disposal that protects your most ignored asset – your own health and well-being.

Financial Needs Hierarchy Pyramid

Bottom Line

Unfortunately, health issues continue to be the leading cause of bankruptcies globally. This is appalling considering the fact that we have had the solution to this problem with us all along – Health Insurance. Yet many of us inadvertently end up underestimating the probability of a health issue occurring and the medical costs associated with it. Health insurance is critical to ensure your loved ones and yourself have the necessary support, if and when they might need it, and the insurance cost is a small price to pay for that assurance. Take action now.