Borrowing can be a powerful tool to boost one’s finances if used in the right way – as discussed in our recent post. We have also explored the other end of the spectrum, that is – borrowing beyond your means and its impact on your cash flow – in our post on how much loan is too much. This article focuses on another important metric that evaluates your assets and liabilities, to make sure you don’t fall into the debt trap. This is the solvency ratio, which tells you how manageable your debt burden is in relation to your assets.

Solvency Ratio

Mathematically speaking, solvency ratio is your net worth (assets – liabilities) divided by your total assets. It indicates how healthy your net worth is as a percentage of your assets. This ratio helps to analyze the ability of individuals to pay off existing debts using existing assets in the event of an unforeseen event.

Solvency Ratio = (Net Worth / Assets) x 100

Example: Let us say Raj has the following financials:

Assets:

Home: Rs 50,00,000

Investments: Rs 20,00,000

Cash: Rs 5,00,000

Total Assets = Rs 75,00,000

Liabilities:

Mortgage: Rs 30,00,000

Car loan: Rs 2,00,000

Credit card loan: Rs 1,00,000

Total Liabilities = Rs 33,00,000

Net Worth = Total Assets – Total Liabilities = Rs 42,00,000

Solvency Ratio = (42,00,000 / 75,00,000) x 100 = 56%

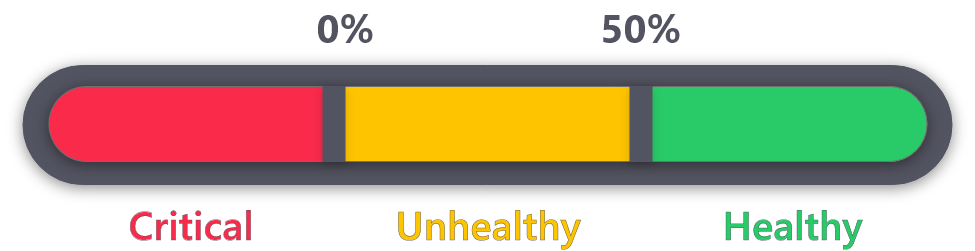

How much should the solvency ratio be?

Solvency ratio should ideally be 50% or above. Anything below that is considered low. Negative values are considered critically low.

What does the solvency ratio tell you?

Having a high solvency ratio indicates a healthy split between assets and liabilities and means that you are well prepared to deal with emergencies and financial downturns. On the other hand, a low solvency ratio is indicative of too much borrowing in relation to your assets. This means that in case of emergencies, you might not be able to pay-off your loans as comfortably.

Such a situation can occur if your assets have reduced in value in conjunction to your loans or due to a large amount of unsecured debt:

Reduction in value of assets: In case your assets reduce in value due to a downturn, you might see your loans outgrowing your asset prices. A good example of this is the subprime mortgage crisis of 2008. House prices fell sharply, dwarfing the prices in comparison to the mortgage amounts. The best way to combat such situations is to keep your portfolio diversified among different asset classes, so that other assets can come to the rescue for downturns in certain areas.

Large amount of unsecured debt: This means that the person has not only been borrowing against the assets that they own, but also getting significant amounts of unsecured loans without any collaterals. These loans, if large enough, can affect your ability to pay off your debts during emergency situations. Hence, it’s advisable to always limit your unsecured borrowings to manageable amounts using the solvency ratio as a guide.

Implication of solvency ratio on insurance

We have talked about the importance of risk management with respect to your finances and why life insurance is critical in this regard. The implication of solvency ratio comes into the picture with regards to dependants, if one were to pass on. For someone with a low or negative solvency ratio, the dependants will struggle to pay off the outstanding debt with the remaining assets. This debt burden will cripple their finances and ability to sustain their current standard of living. Having an insurance that at least covers your liabilities, helps address some of the major concerns in this situation. In addition, maintaining a healthy solvency ratio ensures that immediate liquidation of assets is not needed upon the passing of the debtor.

Bottom Line

It is important to use debt in order to leverage the power of your funds to reach your goals. However, you must be cognizant of how much leverage is beneficial and how much is too much. This is where solvency ratio acts as a good guide and helps ensure that you are well prepared for life’s uncertainties.