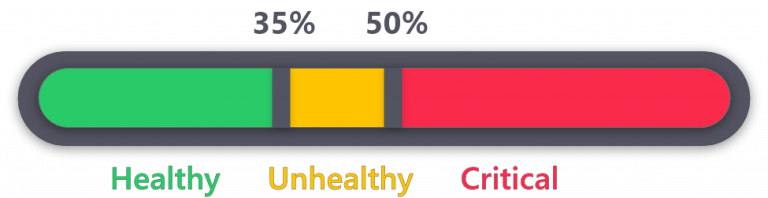

There are certain unique situations, where an increase in the debt servicing ratio is acceptable, while still keeping it away from critical levels. For example, if you have high interest loans such as credit card loan or personal loan, it might be advisable to increase the EMI amounts, so that you can pay up the loans sooner and save on interest costs.