Key Takeaways

- Financial Reviews Are Vital: A year-end review helps you evaluate your financial health and set the stage for a better year ahead.

- Maximize Tax Savings: Ensure you’ve fully utilized tax-saving options like ELSS, NPS, or 80C deductions.

- Prepare for Big Goals: Start planning for significant expenses or investments in the coming year.

- Reassess Insurance and Emergency Funds: Make sure you have adequate coverage and a robust safety net in place.

As December rolls around, the holiday season isn’t just a time for celebrations—it’s also the perfect moment to give your finances a thorough review. Think of it as closing the books on the year gone by while preparing for a fresh start. Here’s a relatable, easy-to-follow financial checklist to help you take stock and plan for a stronger financial future.

Why Is a Year-End Financial Review Important?

Think of a year-end financial review as your financial health checkup. Just like an annual medical check ensures you’re physically fit, reviewing your finances helps you evaluate how well you’re doing financially and prepare for what’s ahead.

It allows you to identify gaps—be it missed tax-saving opportunities, inadequate savings, or unoptimized investments.

This process ensures you’re on track to meet your financial goals while also protecting yourself from unexpected shocks, like market downturns or emergencies. Without this yearly reflection, you risk starting the new year with unresolved financial issues, making it harder to achieve long-term stability and growth.

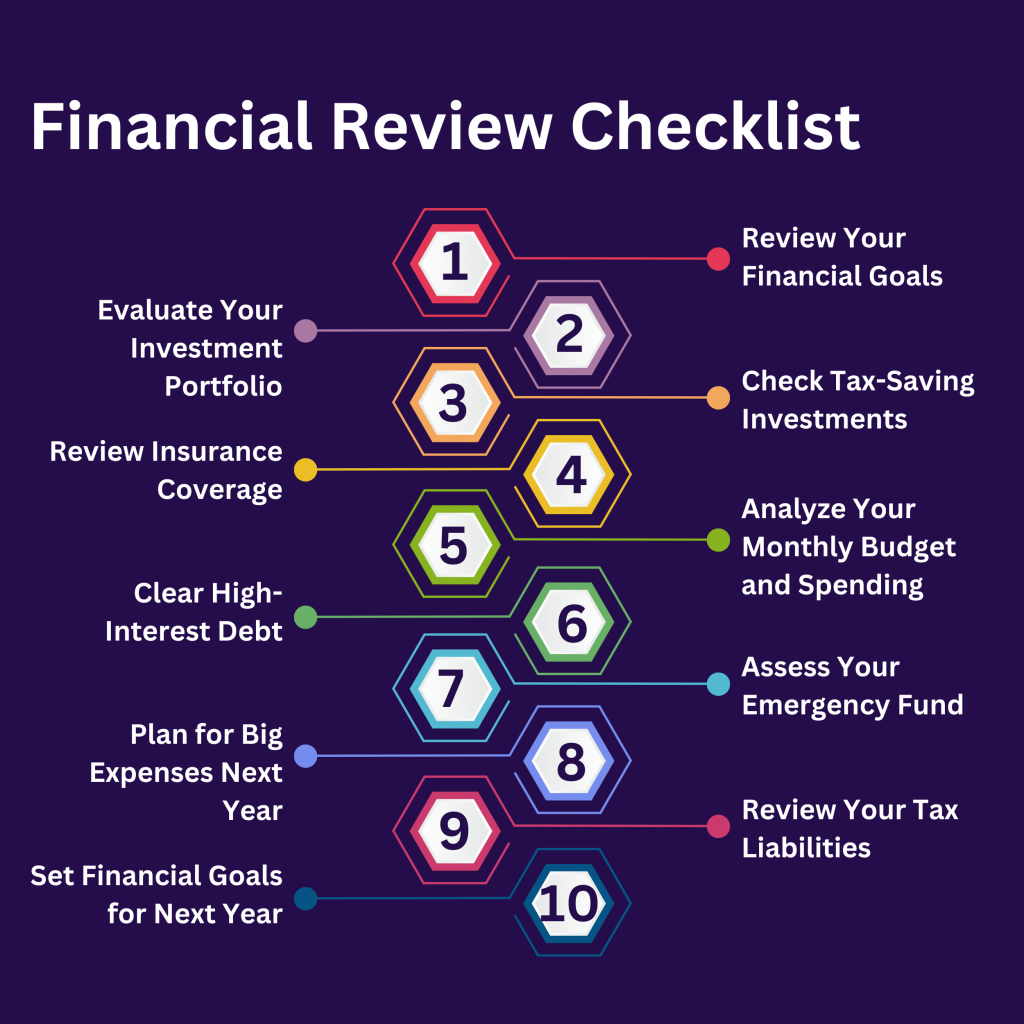

1. Review Your Financial Goals

Start with the big picture. Did you meet the financial goals you set for yourself this year? Maybe it was saving for a vacation, paying off debt, or starting an SIP.

Example:

Riya, a 29-year-old software engineer, planned to save ₹1.2 lakhs this year. By reviewing her savings, she realized she was short by ₹20,000 because of unexpected expenses. This review helped her reassess her budget for next year.

2. Evaluate Your Investment Portfolio

Take a look at your equity, mutual funds, or other investments. Has your portfolio drifted from your planned allocation? Rebalancing can ensure your investments align with your risk tolerance and goals.

Tip:

If you notice underperforming investments, consider switching to better options. Tools like Cashvisory can guide you here.

3. Check Tax-Saving Investments

Ensure you’ve maximized deductions under Section 80C (₹1.5 lakhs) or other sections like 80D (for health insurance). Tax-saving mutual funds (ELSS), PPF, or NPS can help reduce your tax burden while growing your wealth.

Example:

Arjun, a marketing professional, realized in December he hadn’t fully utilized his 80C limit. He invested ₹50,000 in an ELSS fund to save taxes and grow his savings.

4. Review Insurance Coverage

Term insurance is a critical financial safeguard. Ensure your coverage is adequate and meets current needs. For instance, a salary increase or a new family member may call for additional coverage.

Tip:

If you don’t have term insurance, now’s a great time to explore options.

5. Analyze Your Monthly Budget and Spending

Look back at your spending habits. Were there months where you overspent? Identifying patterns can help you create a more realistic budget for the next year.

Example:

Priya, a teacher, noticed she overspent on dining out during festivals. She resolved to allocate a separate budget for such occasions next year.

6. Clear High-Interest Debt

Check outstanding credit card balances or personal loans. Paying off high-interest debt should be a priority to avoid unnecessary financial stress.

Tip:

If paying off entirely isn’t possible, try to refinance or consolidate debt for a lower interest rate.

7. Assess Your Emergency Fund

Ideally, you should have 3-6 months’ worth of expenses saved in an emergency fund. If you dipped into it this year, now is the time to replenish it.

Example:

Ravi, a graphic designer, used ₹50,000 from his emergency fund for unexpected home repairs. He decided to rebuild this fund by setting aside ₹5,000 every month starting January.

8. Plan for Big Expenses Next Year

Are you planning a wedding, buying a car, or going on an international vacation? Start earmarking funds for these big-ticket items now to avoid last-minute financial stress.

9. Review Your Tax Liabilities

Estimate your tax liability for the financial year ending in March. This is also the time to check if you’ve made necessary advance tax payments to avoid penalties.

Tip:

Use December to gather investment proof for your employer and streamline the tax filing process.

10. Set Financial Goals for Next Year

Whether it’s starting an SIP, saving for a down payment, or creating a new income source, set clear and measurable financial goals for the year ahead.

Cashvisory: Simplifying Year-End Financial Planning

Year-end financial reviews can feel overwhelming, but platforms like Cashvisory make it easier. Here’s how:

- Portfolio Insights: Get a detailed view of your investments and actionable rebalancing suggestions.

- Tax Optimization Tools: Identify missed opportunities to save taxes and plan better for next year.

- Goal-Based Planning: Set and track customized financial goals with expert guidance.

- Emergency Fund Builder: Use tailored saving strategies to replenish or grow your safety net.

Take the guesswork out of financial planning—start your year-end review with Cashvisory’s tools and support. Sign up for a free consultation call today!

By following this checklist, you’ll not only close this year on a financially sound note but also set yourself up for success in the coming year. Remember, a little planning today can lead to significant rewards tomorrow!