Key Takeaways

- Understanding Differences: Learn the core differences between term insurance and whole life insurance.

- Cost-Effectiveness: Discover why term insurance is often a more cost-effective option.

- Investment Potential: See how savings from lower premiums on term insurance can be invested for greater wealth accumulation.

- Maximizing Returns: Explore how choosing the right insurance can enhance your investment strategy and overall financial health.

Introduction

Choosing the right type of insurance is crucial for building and securing your financial future. Insurance plays a vital role in wealth-building by providing financial protection and enabling you to allocate more resources toward investments. Among the various insurance options, term insurance and whole life insurance are commonly considered. While both offer benefits, term insurance often emerges as the more effective choice for maximizing your wealth. This article will explore the differences, benefits, and strategic advantages of opting for term insurance, and how Cashvisory helps you select the best products and strategies to enhance your wealth-building potential.

What is Term Insurance?

Term insurance provides coverage for a specific period, usually ranging from 10 to 30 years. If the policyholder passes away during this term, the beneficiaries receive the death benefit. However, if the policyholder survives the term, there is no payout. Term insurance is akin to renting a safety net for your family’s financial security for a defined period.

What is Whole Life Insurance?

Whole life insurance, on the other hand, offers lifelong coverage. It combines a death benefit with a savings component, known as the cash value, which grows over time. This type of policy is more like owning a house where you build equity over the years.

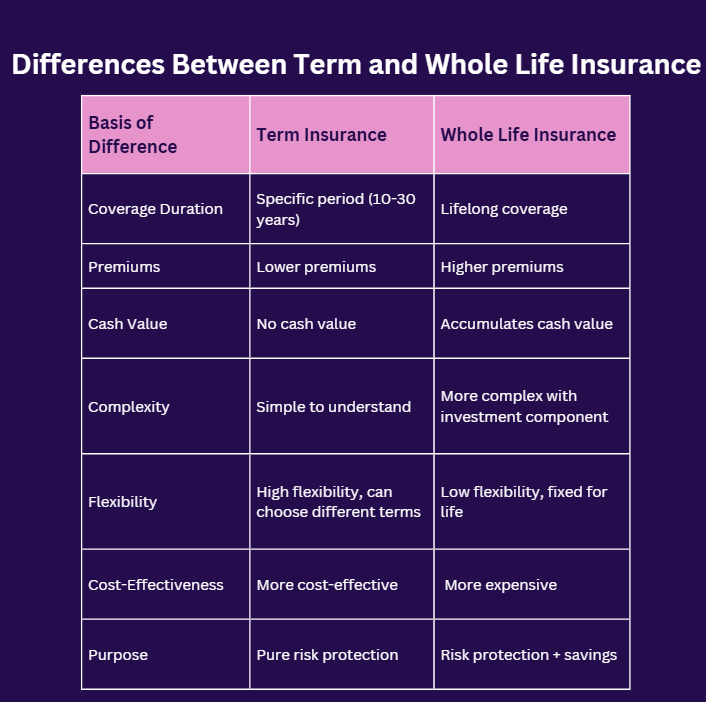

Differences Between Term and Whole Life Insurance

| Basis of Difference | Term Insurance | Whole Life Insurance |

| Coverage Duration | Specific period (10-30 years) | Lifelong coverage |

| Premiums | Lower premiums | Higher premiums |

| Cash Value | No cash value | Accumulates cash value |

| Complexity | Simple to understand | More complex with investment component |

| Flexibility | High flexibility, can choose different terms | Low flexibility, fixed for life |

| Cost-Effectiveness | More cost-effective | More expensive |

| Purpose | Pure risk protection | Risk protection + savings |

Why Term Insurance is a Better Option

1. Cost-Effectiveness

Term insurance premiums are significantly lower than whole life insurance premiums. This means you can get higher coverage for a lower cost.

Example

A 30-year-old non-smoker might pay INR 15,00 per month for a 1 cr term policy, but over INR 15,000 per month for a whole life policy with the same coverage.

2. Investment Potential

The money saved on premiums can be invested elsewhere to generate higher returns.

Scenario

If you save INR 13500 per month by choosing term insurance over whole life insurance, you could invest that money in mutual funds or stocks. Over 20 years, assuming an average annual return of 7%, you could accumulate a substantial corpus.

Example

Consider Sarah, a 35-year-old mother of two. She opts for a 20-year term insurance policy with a ₹1 crore death benefit for ₹1,500 per month. Instead of choosing a whole life policy costing ₹15,000 per month, she saves ₹13,500 monthly. Sarah invests these savings using Cashvisory, which helps her build a diversified investment portfolio. Over 20 years, her investment grows to approximately ₹73,56,000, assuming a 6% annual return.

In contrast, a whole life insurance policy with a similar coverage and premium of ₹15,000 per month might offer a surrender value around ₹50,00,000 to ₹60,00,000 after 20 years. While this includes the insurance coverage and a cash value component, the amount you can accumulate through strategic investing with term insurance is significantly higher. This comparison illustrates how choosing term insurance and investing the savings can lead to greater wealth accumulation.

How Cashvisory Can Help

Cashvisory provides comprehensive support in selecting the right insurance policy that aligns with your financial goals and wealth-building strategy. Our insurance advisory services help you evaluate the benefits of term insurance versus whole life insurance, ensuring you make an informed choice that suits your needs and budget. Once you opt for term insurance and save on premiums, Cashvisory’s platform steps in to assist you in investing these savings effectively. We offer tailored investment solutions that help you build a diversified portfolio, optimizing your wealth accumulation over time. By integrating insurance with strategic investment planning, Cashvisory ensures that all aspects of your financial health are managed comprehensively, helping you achieve your long-term financial goals efficiently.

Conclusion

Opting for term insurance over whole life insurance can be a strategic move for those looking to maximize their wealth. Lower premiums mean more money to invest in high-yield assets, potentially growing your wealth significantly over time. With Cashvisory’s comprehensive approach, we provide expert guidance to help you choose the best insurance products for your needs and ensure that the savings from lower premiums are effectively invested. Our personalized support, educational resources, and hands-on advice are designed to help you navigate both insurance choices and investment decisions, maximizing your wealth-building potential.