When it comes to investing, hidden fees are often like a slow leak—barely noticeable but capable of draining your returns over time. These fees, embedded in many investment products, can significantly affect your portfolio’s growth. Whether you’re investing in mutual funds, stocks, or other vehicles, understanding these hidden costs is crucial to maximizing returns.

Key takeaways

- Hidden Fees Matter: Fees like expense ratios, transaction costs, and advisory fees can significantly reduce your returns over time.

- Active vs. Passive Funds: Actively managed funds typically have higher fees compared to passive index funds.

- Direct vs. Traditional Plans: Direct mutual funds have lower expense ratios and are more cost-effective than traditional funds.

- How to Minimize Fees: Opt for no-fee brokers, low-cost index funds, and a buy-and-hold strategy to reduce overall costs.

- Read the Fine Print: Always scrutinize the fee structure of any investment to avoid surprises.

The Real Impact of Hidden Fees

Imagine investing ₹5,00,000 in a mutual fund with an expected return of 10% annually. If the expense ratio is 2%, your effective return would be just 8%. While 2% might not seem like much, compounded over 20 years, this could mean losing over ₹3,00,000 in returns. This is similar to running a marathon with a small weight attached to your back—every mile gets harder, and the finish line seems further away.

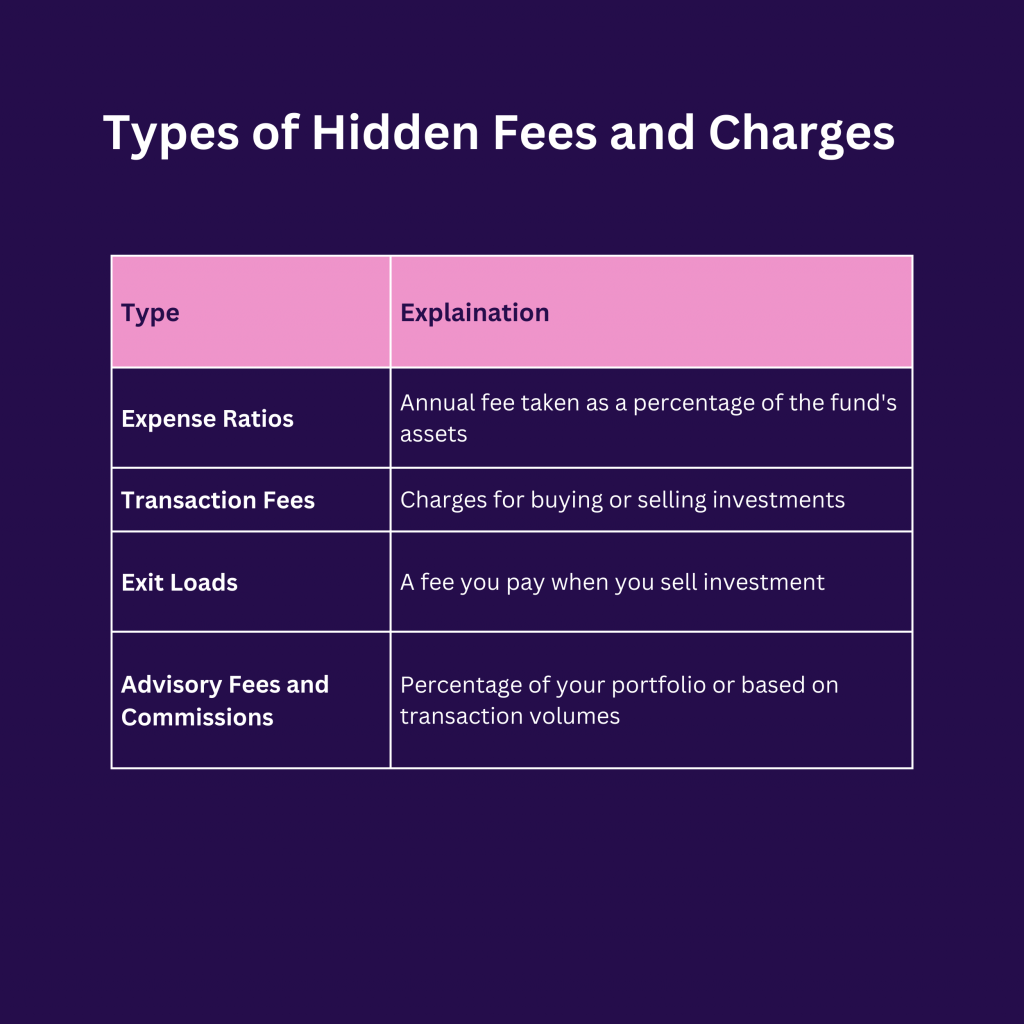

Types of Hidden Fees and Charges

There are several hidden fees investors should be aware of:

- Expense Ratios: An annual fee taken as a percentage of the fund’s assets, common in mutual funds. The higher the ratio, the more it erodes your returns.

- Transaction Fees: Charges for buying or selling investments, especially in actively traded portfolios.

- Exit Loads: A fee you pay when you withdraw from a mutual fund within a specified time frame.

- Advisory Fees and Commissions: These are charged by brokers or financial advisors, typically as a percentage of your portfolio or based on transaction volumes.

- Active vs. Passive Management: Actively managed funds tend to charge higher fees due to frequent trading and hands-on management. Passive funds, like index funds, usually have much lower fees, since they aim to match the market rather than outperform it.

Traditional vs. Direct Funds: Why Expense Ratios Matter

Both traditional and direct mutual funds are identical in terms of asset allocation and investment strategy. However, traditional funds come with higher expense ratios due to distribution costs, while direct funds are cheaper because they eliminate intermediaries. Over time, choosing a lower expense ratio can lead to better long-term gains.

How Fees Eat Into Your Returns

Let’s break it down further. Say you invest ₹10,00,000 in two different mutual funds—one with a 1.5% expense ratio and another with a 0.5% ratio. Assuming both generate 10% returns annually, after 10 years, the higher-cost fund will have earned around ₹14,000 less than the lower-cost one. This difference only grows as your investment horizon extends, highlighting the importance of scrutinizing fees.

Ways to Minimize These Costs

- Buy-and-Hold Strategy: A simple yet effective way to minimize transaction fees. By holding onto investments longer, you avoid frequent trading costs.

- Choose No-Load Mutual Funds: These funds don’t charge sales commissions, reducing your overall expenses.

- Utilize Low-Cost Index Funds: Index funds often have lower expense ratios compared to actively managed funds, making them a cost-effective option.

- Opt for Direct Funds: When choosing mutual funds, go for direct plans as they offer the same portfolio with a lower expense ratio.

How Can I Avoid Investment Fees?

To minimize investment fees, start by focusing on saving on brokerage fees and commissions. Opt for no-fee brokers, as many online platforms now offer commission-free trades for stocks and ETFs. This can help you avoid the compounding effect of commissions, where even small fees can snowball and erode your returns over time.

Another strategy is to work with flat-fee advisors instead of those who charge based on transactions or commissions. The problem with commission-based advisors or distributors is the conflict of interest—they are often incentivized to push products with higher commissions rather than those that are best suited for your financial goals. Flat-fee advisors, on the other hand, charge a set amount, regardless of the products they recommend, aligning their incentives more closely with your interests.

Why Professional Guidance Can Help

While reducing fees is essential, professional guidance can still be invaluable. A Registered Investment Advisor (RIA), like Cashvisory, offers transparent, flat-fee services and is legally obligated to act in your best interest. This ensures that the focus remains on your financial growth, not on earning commissions from specific products. By working with an RIA, you can navigate complex fee structures more effectively and avoid costly investment traps.

RIAs provide personalized advice, helping you select low-cost investment options that align with your long-term goals. Their flat-fee model removes the potential conflicts of interest found with commission-based advisors, ensuring your money works for you—not for them.

The Role of Registered Investment Advisors (RIAs) in Managing Investment Costs

Working with a Registered Investment Advisor (RIA) can help you navigate the complexities of investment fees and commissions. RIAs are legally obligated to act in your best interest, which means they are transparent about the costs involved in your investment choices, including expense ratios and hidden fees. Unlike brokers who may earn commissions from the products they sell, RIAs typically operate on a fee-only model, minimizing conflicts of interest and ensuring you receive unbiased advice. By consulting an RIA, you can better understand the true costs of your investments and make more informed decisions that align with your financial goals.

Conclusion

Hidden fees are a silent threat to your long-term wealth. By educating yourself on the different types of fees and adopting strategies to minimize them, you can ensure more of your money stays invested. Always read the fine print, choose low-cost options when possible, and consider professional guidance to navigate the complex world of investment fees.

Your returns shouldn’t just pay the managers—they should work for you.