Key Takeaways

- Portfolio Drift Happens: Market movements can skew your asset allocation, increasing your risk exposure.

- Rebalancing Is Risk Management: It ensures your portfolio aligns with your financial goals and risk tolerance, even during market volatility.

- Timing Matters: Rebalancing periodically or based on significant allocation shifts (5-10%) is essential to stay on track.

- Simplified Solutions Exist: Tools like robo-advisors and platforms like Cashvisory can make rebalancing easier and more efficient.

- Avoid DIY Stress: Partnering with experts minimizes errors, saves time, and ensures tax-efficient rebalancing.

Picture this: You set out on a road trip with your car perfectly aligned. But over time, the tires wear unevenly, making the ride bumpier. You risk losing control if you don’t realign. The same principle applies to your investment portfolio—it needs periodic rebalancing to stay aligned with your goals, especially during market turbulence.

Let’s explore why rebalancing your portfolio is a must during volatile times and how you can approach it effortlessly.

Understanding Equity-Debt Ratios: What Do 60:40 or 70:30 Mean?

The 60:40 or 70:30 equity-debt ratio refers to how your investment portfolio is divided between equity (stocks or mutual funds) and debt (bonds or fixed-income instruments). Equity is growth-oriented but riskier, while debt provides stability and lower risk. For instance, a 60:40 ratio means 60% of your money is invested in equities and 40% in debt, balancing growth potential with risk management based on your financial goals and risk tolerance.

Why Does Your Portfolio Drift?

Imagine you start with a balanced portfolio—50% in equity and 50% in debt, with an initial investment of ₹10 lakhs (₹5 lakhs each in equity and debt). Over time, during a bull market, equity grows by 20%, reaching ₹6 lakhs, while debt grows by 5%, increasing to ₹5.25 lakhs. Now, your total portfolio value is ₹11.25 lakhs, but the allocation has shifted to approximately 53% equity (₹6 lakhs) and 47% debt (₹5.25 lakhs).

While this slight drift might not seem alarming, let’s say equity grows even faster, reaching ₹8 lakhs in the next cycle, while debt remains at ₹5.25 lakhs. Your portfolio now totals ₹13.25 lakhs, but the allocation has shifted significantly to 60% equity and 40% debt.

Without rebalancing, this drift exposes your portfolio to higher risk, as equities are more volatile than debt. If a market correction occurs, the heavy equity allocation could lead to a larger-than-expected loss, making your portfolio misaligned with your original goals and risk tolerance.

Why Is Rebalancing Crucial?

1. Risk Management

Market volatility can skew your portfolio allocation. Rebalancing ensures you don’t take on unintended risks.

Example:

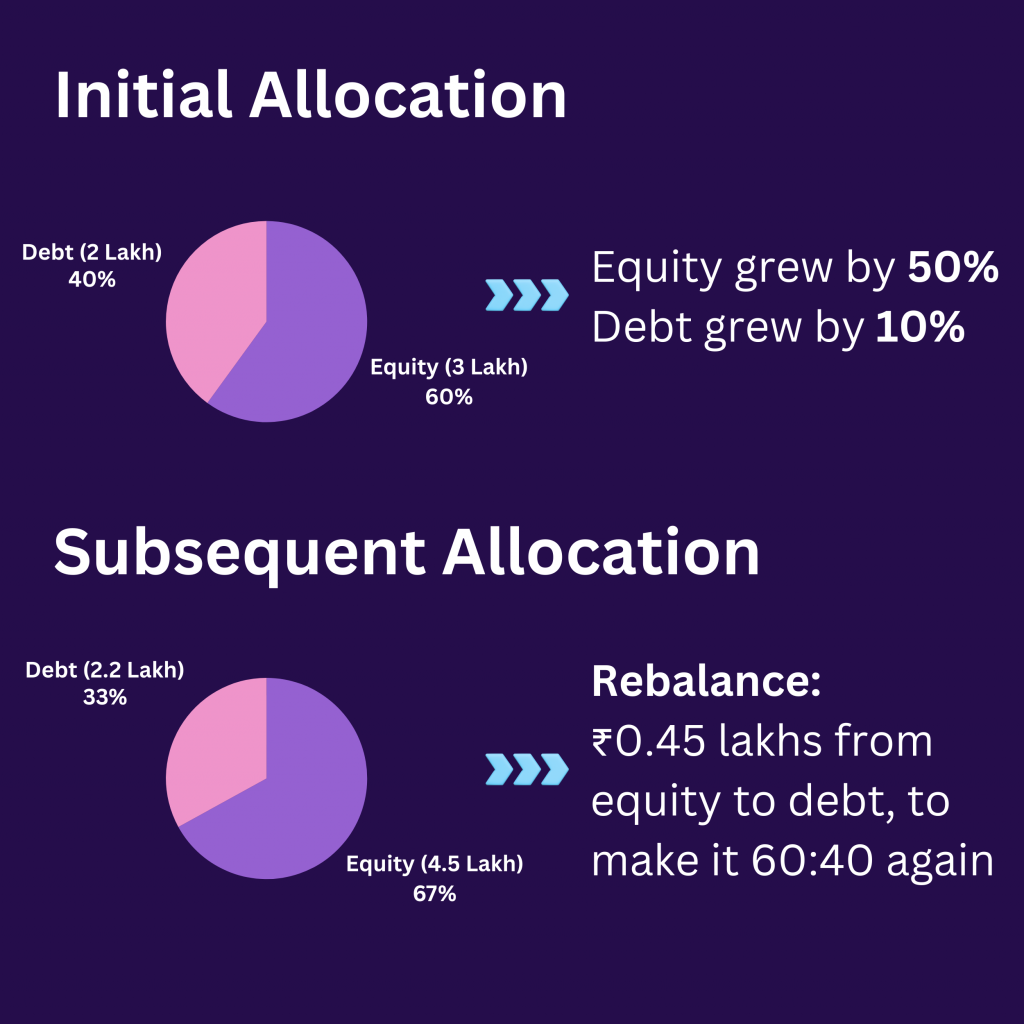

Ravi, 30, started investing ₹5 lakhs in 2020 with a 60:40 equity-to-debt portfolio:

- Equity: ₹3 lakhs

- Debt: ₹2 lakhs

By 2023, due to a booming equity market, his equity grew by 50%, reaching ₹4.5 lakhs, while debt grew by 10%, increasing to ₹2.2 lakhs. His total portfolio value became ₹6.7 lakhs, but the allocation shifted to approximately 67% equity (₹4.5 lakhs) and 33% debt (₹2.2 lakhs).

When markets corrected in 2024 and equity dropped by 15%, his equity value fell to ₹3.83 lakhs, while debt remained stable at ₹2.2 lakhs. His total portfolio value declined to ₹6.03 lakhs. If Ravi had rebalanced earlier, restoring the 60:40 ratio, he could have shifted ₹0.45 lakhs from equity to debt, reducing his losses during the downturn.

This highlights how rebalancing can help manage risk and protect your portfolio from unexpected market corrections.

2. Staying on Track with Goals

Your portfolio is built around goals like buying a house or retiring early. Drifting from your original allocation can derail your financial plan.

Example:

Let’s say you aim to build a ₹50 lakh corpus in 20 years with a 60:40 equity-to-debt portfolio. You start with ₹10 lakhs:

- Equity: ₹6 lakhs (expected to grow at 12% annually)

- Debt: ₹4 lakhs (expected to grow at 6% annually).

If you rebalance periodically, your portfolio grows as planned, and you achieve your target of ₹50 lakhs. But without rebalancing, if equity performs exceptionally and grows to 80% of your portfolio within a few years, you face higher risk exposure.

In a downturn, if equities lose 20% value during a market correction, your portfolio may drop significantly—leaving you with ₹38-40 lakhs instead of your target. This shortfall could delay your goal, whether it’s buying a house or retiring comfortably.

Rebalancing helps ensure your investments remain aligned with your financial objectives, minimizing such risks.

3. Locking in Profits

Rebalancing lets you sell high-performing assets and reinvest in underperforming ones, effectively “buying low and selling high.”

Example:

Let’s assume you start with ₹10 lakhs in a 70:30 equity-to-debt portfolio:

- Equity: ₹7 lakhs

- Debt: ₹3 lakhs

During a market rally, equity grows by 30%, increasing to ₹9.1 lakhs, while debt grows by 5%, reaching ₹3.15 lakhs. Your portfolio value now stands at ₹12.25 lakhs, and the allocation shifts to 74% equity and 26% debt.

To rebalance back to 70:30, you sell ₹0.35 lakhs worth of equity (at a higher price) and reinvest it into debt (at a lower price). Now, equity is ₹8.75 lakhs (70%) and debt is ₹3.5 lakhs (30%).

When markets later correct and equity drops by 15%, your portfolio remains better protected:

- Without rebalancing: Equity value drops to ₹7.74 lakhs, and the total portfolio value is ₹10.89 lakhs.

- With rebalancing: Equity value drops to ₹7.44 lakhs, but debt remains ₹3.5 lakhs, leaving your total portfolio at ₹10.94 lakhs—a smaller loss.

This example shows how rebalancing helps lock in gains during market highs and protects you during downturns.

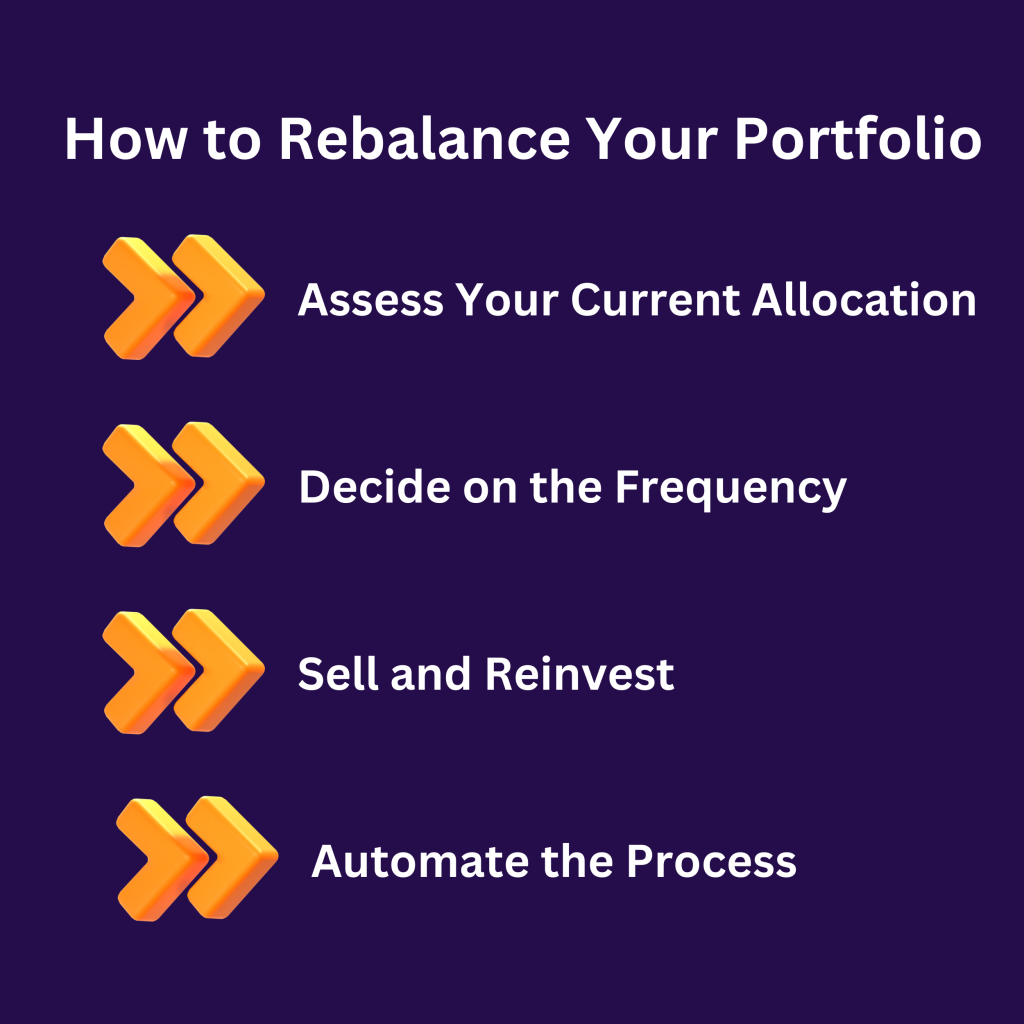

How to Rebalance Your Portfolio

Step 1: Assess Your Current Allocation

Start by reviewing your portfolio. Compare the current allocation to your target allocation.

Step 2: Decide on the Frequency

Rebalancing can be done:

- Annually: Ideal for most long-term investors.

- Trigger-based: When the allocation deviates by 5-10%.

Step 3: Sell and Reinvest

Sell portions of overperforming assets and reinvest in underperforming ones to restore balance.

Step 4: Automate the Process

To avoid the hassle of DIY rebalancing, consider solutions like robo-advisors or professional portfolio management services.

Real-Life Example of Rebalancing

Example:

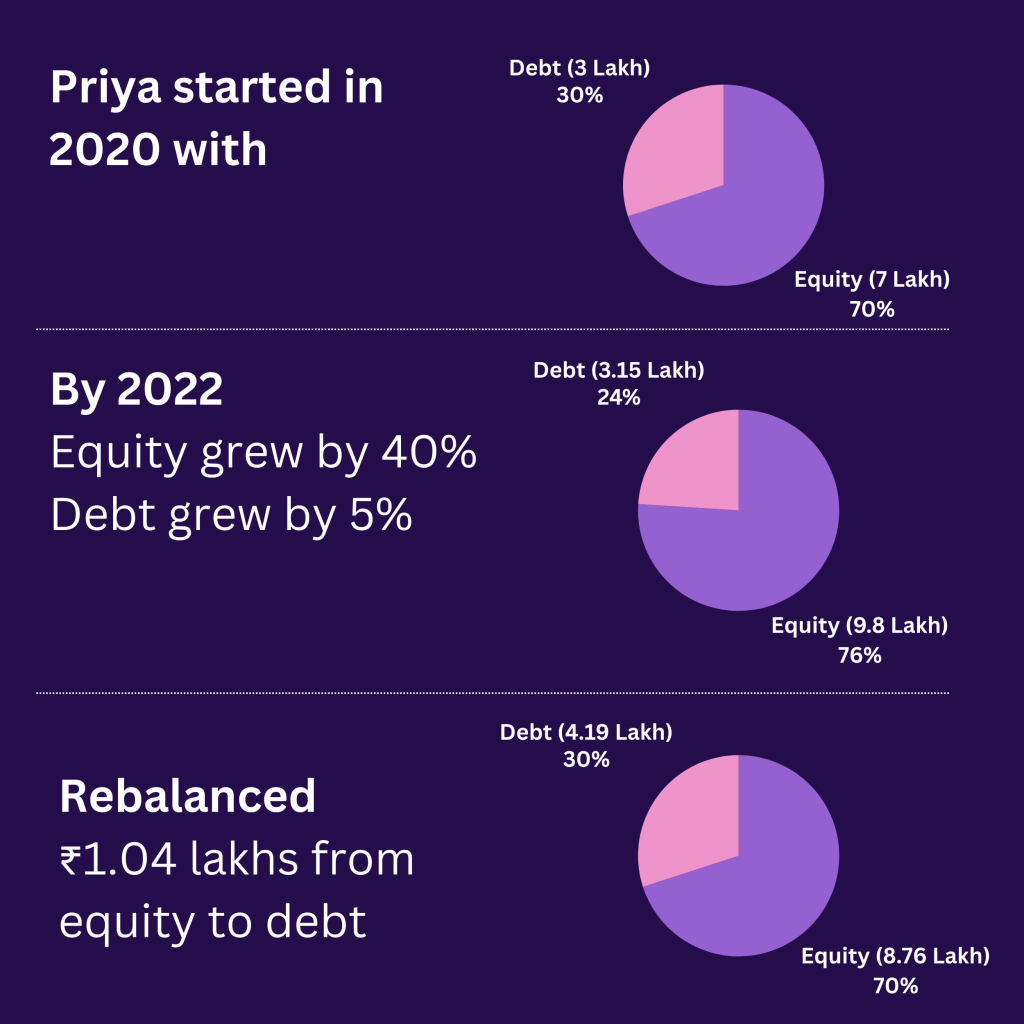

Priya, a 35-year-old IT professional, started with ₹10 lakhs in a 70:30 equity-to-debt portfolio in 2020:

- Equity: ₹7 lakhs

- Debt: ₹3 lakhs

By 2022, during a market rally, her equity grew by 40%, reaching ₹9.8 lakhs, while debt grew by 5%, increasing to ₹3.15 lakhs. Her total portfolio value became ₹12.95 lakhs, with an allocation of approximately 76% equity and 24% debt.

Concerned about increased risk, Priya rebalanced her portfolio back to 70:30. She sold ₹1.04 lakhs of equity, reducing it to ₹8.76 lakhs (70% of ₹12.95 lakhs), and reinvested the amount into debt, increasing it to ₹4.19 lakhs (30% of ₹12.95 lakhs).

When markets declined by 20% in 2023, Priya’s rebalanced portfolio fared better:

- Equity dropped to ₹7.01 lakhs (20% loss on ₹8.76 lakhs).

- Debt remained stable at ₹4.19 lakhs.

- Total portfolio value: ₹11.2 lakhs.

Without rebalancing, her equity-heavy portfolio would have faced a greater loss:

- Equity dropped to ₹7.84 lakhs (20% loss on ₹9.8 lakhs).

- Debt remained at ₹3.15 lakhs.

- Total portfolio value: ₹10.99 lakhs.

By rebalancing, Priya preserved an additional ₹21,000 and reduced her exposure to volatility, proving the importance of periodic portfolio rebalancing.

A Hassle-Free Approach to Rebalancing

Rebalancing might sound like a tedious task—tracking portfolio allocations, deciding what to sell or buy, and ensuring you don’t trigger unnecessary taxes or fees. For busy professionals or those new to investing, this process can be overwhelming. Fortunately, you don’t have to go it alone.

1. Robo-Advisors: Simplifying Rebalancing

Robo-advisors are automated platforms that rebalance your portfolio based on predefined rules. Once you set your risk tolerance and financial goals, they monitor your investments and adjust allocations as needed. While convenient, these platforms might not always offer personalized advice or account for unique situations, like major life changes.

2. Professional Portfolio Management Services

Hiring a professional portfolio manager can provide a hands-on, tailored approach. Experts assess your portfolio, align it with your goals, and rebalance as market conditions change. This approach ensures your investments are actively managed, but it can be costly and less accessible for small investors.

Cashvisory: Your Partner in Smart Rebalancing

At Cashvisory, we aim to make portfolio rebalancing simple, efficient, and tailored to your needs. Here’s how we help:

- Personalized Portfolio Review: We evaluate your current portfolio, identifying any imbalances or risks that need attention.

- Goal-Oriented Strategies: Unlike one-size-fits-all solutions, we align rebalancing decisions with your specific goals, whether it’s early retirement, buying a house, or building an emergency fund.

- Expert Guidance: Our financial advisors take the guesswork out of rebalancing. They provide clear recommendations on what to buy, sell, or hold based on market conditions and your financial plan.

- Technology + Human Touch: Using our platform, you can easily track your portfolio and consult with experts to determine when rebalancing may be required.

- Tax Loss Harvesting (Opt-in): For those who opt in, we help minimize tax liabilities by strategically selling underperforming assets to offset gains, ensuring better post-tax returns.

Why Choose Cashvisory?

- Ease of Use: With user-friendly tools and dashboards, you can monitor your portfolio anytime.

- Affordable Subscription Plans: Our subscription plans are designed to be cost-effective, making advanced portfolio management, including rebalancing, accessible to everyone, whether you’re a beginner or a seasoned investor.

- Ongoing Support: Need help? Our advisors are just a call away to assist you at every step.

By partnering with Cashvisory, you can stop worrying about market swings and portfolio drifts. Instead, you’ll have a trusted ally to keep your investments on track, so you can focus on achieving your financial dreams.

Conclusion: A Steady Ride to Financial Independence

Just like maintaining your car, rebalancing your portfolio periodically ensures a smoother journey toward your financial goals. By managing risk, staying goal-focused, and automating the process, you can confidently navigate volatile markets.

Take the first step today—evaluate your portfolio and explore solutions to make rebalancing stress-free!