Key Takeaways

- Start Early: Don’t wait until the last minute to plan your taxes; early planning allows better investment choices.

- Use Section 80C Effectively: Max out the ₹1.5 lakh limit with options like ELSS, PPF, and NPS.

- Think Long-Term: Choose tax-saving investments that also align with your long-term goals, like retirement or wealth building.

- Diversify Investments: Balance between high-return instruments (ELSS) and safe options (PPF or SSY) for stability and growth.

- Health Insurance Benefits: Utilize Section 80D deductions for self and family to save taxes while ensuring financial security.

As the calendar year draws to a close, December becomes a crucial month for reviewing finances and submitting investment proofs to HR. While the financial year officially ends in March and tax filing deadlines extend to July, starting your tax planning now ensures smarter decisions, aligning your investments with financial goals and long-term wealth creation.

Smart tax planning is not just about saving money; it’s about aligning your financial goals with long-term wealth creation. In this article, we’ll break down practical, actionable strategies for effective year-end tax planning using popular investment options under Section 80C and other provisions of the Indian Income Tax Act.

Why Year-End Tax Planning Matters

Waiting until the last moment can lead to rushed decisions and suboptimal investments. Proper tax planning ensures that:

- You maximize deductions to save taxes.

- Your investments align with your financial goals (e.g., retirement or buying a home).

- You build wealth over time while meeting statutory requirements.

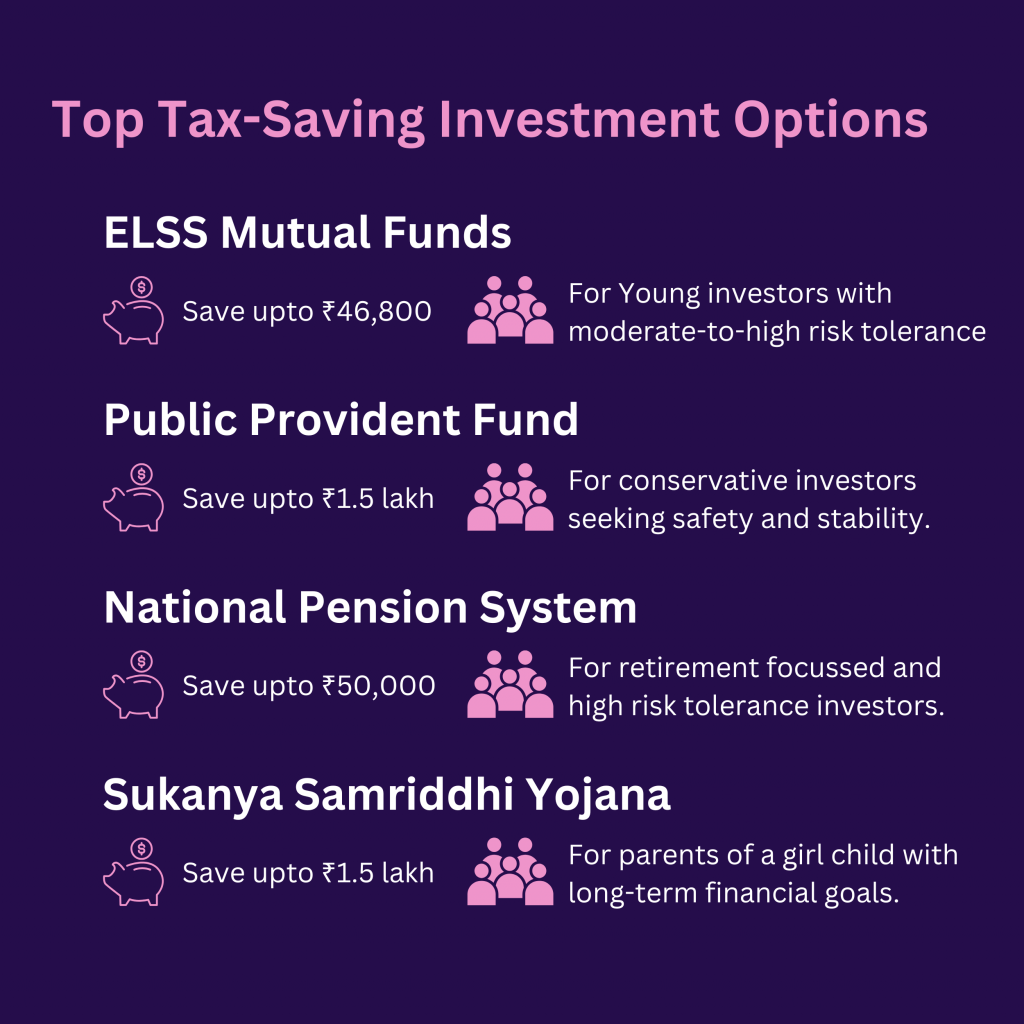

Top Tax-Saving Investment Options

1. ELSS Mutual Funds (Equity-Linked Savings Schemes)

ELSS offers tax savings under Section 80C and high growth potential with the shortest lock-in period of 3 years.

- Tax Savings: Up to ₹46,800 (if you invest ₹1.5 lakh and fall under the 30% tax bracket).

- Lock-In Period: 3 years (shortest under Section 80C).

- Who Should Invest: Young investors with moderate-to-high risk tolerance.

- Example: Invest ₹1.5 lakh; potential corpus after 3 years = ₹2.11 lakh (12% annualized return).

2. Public Provident Fund (PPF)

A risk-free, government-backed option for long-term goals like retirement. Offers stable, tax-free returns.

- Tax Savings: Deduction up to ₹1.5 lakh under Section 80C.

- Lock-In Period: 15 years (partial withdrawals allowed after 7 years).

- Who Should Invest: Conservative investors seeking safety and stability.

- Example: Annual investment of ₹1.5 lakh; grows to ₹40 lakh in 15 years (7.1% interest).

3. National Pension System (NPS)

A market-linked retirement savings tool offering additional tax benefits.

- Tax Savings: Up to ₹50,000 under Section 80CCD(1B) (over and above ₹1.5 lakh under 80C).

- Lock-In Period: Till retirement (60 years of age); partial withdrawals allowed.

- Who Should Invest: Individuals focused on retirement planning with higher risk tolerance.

- Example: Invest ₹50,000 annually; grow to ₹50 lakh+ in 25 years (10% return). Save ₹15,600 annually in taxes (30% tax bracket).

4. Sukanya Samriddhi Yojana (SSY)

A secure, tax-efficient option for the financial security of a girl child.

- Tax Savings: Up to ₹1.5 lakh under Section 80C.

- Lock-In Period: Until the child turns 21 (minimum 15 years of contributions).

- Who Should Invest: Parents of a girl child with long-term financial goals.

- Example: Invest ₹1.5 lakh annually for 15 years; corpus grows to ₹63 lakh (8% interest).

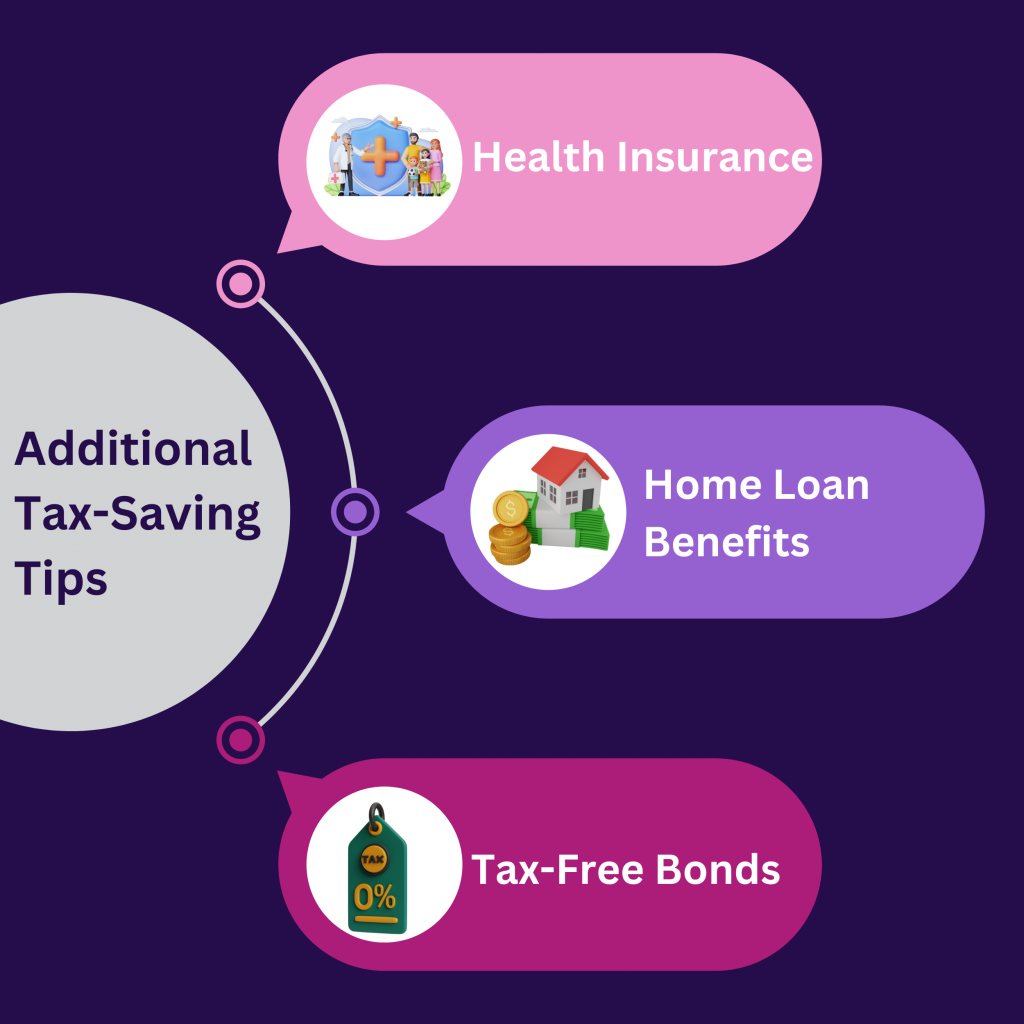

Additional Tax-Saving Tips

- Health Insurance (Section 80D): Premiums up to ₹25,000 for self and ₹50,000 for senior citizen parents are tax-deductible.

- Home Loan Benefits (Section 24B and 80C): Deduct interest on home loans (up to ₹2 lakh annually) and principal repayment (part of 80C).

- Tax-Free Bonds: Though not under 80C, these offer tax-free interest and are ideal for low-risk, fixed-income investments.

How Tax Deduction Limits Work

Total deductions under Section 80C, 80CCC (pension plans), and 80CCD(1) (NPS Tier 1) are capped at ₹1.5 lakh.

However, Section 80CCD(1B) allows an additional ₹50,000 for NPS, increasing the maximum possible deduction to ₹2 lakh annually.

How Smart Tax Planning Aligns with Wealth Building

Strategic tax planning ensures your money works harder for you. For instance, a salaried professional earning ₹10 lakh annually can reduce their taxable income by leveraging 80C, 80D, and 80CCD deductions, potentially saving ₹70,000–₹1 lakh in taxes.

This saved amount, when invested in growth-oriented funds like ELSS, can compound significantly over time, creating a robust wealth corpus.

Why Choose Cashvisory for Tax Planning?

At Cashvisory, we simplify your financial journey with:

- Investment Optimization: Our expertise lies in guiding you through ELSS investments and tax-loss harvesting, helping you optimize your portfolio for tax savings while aligning with your long-term wealth-building goals.

- Comprehensive Insights: Track, analyze, and optimize your portfolio effortlessly.

Conclusion

Year-end tax planning is not just about saving money; it’s about building a strong financial foundation. By leveraging tools like ELSS, PPF, and NPS, you can reduce your tax burden and grow wealth simultaneously.

Take control of your taxes and investments today with Cashvisory—your partner in achieving financial independence. Start Planning Now!

Frequently Asked Questions (FAQs)

Ready to simplify your year-end tax planning? Explore Cashvisory Now!