Key Takeaways

- Foundation of Financial Planning: Life insurance is a crucial part of a comprehensive financial strategy.

- Types of Life Insurance: Understanding term and permanent life insurance helps in making informed decisions.

- Factors Affecting Premiums: Age, health, lifestyle, and policy type impact the cost of life insurance.

- Benefits of Life Insurance: Protecting loved ones, saving taxes, and securing the future are key benefits.

- Guidance and Considerations: Tips on assessing your insurance needs and steps to take before purchasing a policy.

Introduction

At some point in life, you’ve probably encountered someone trying to sell you an insurance policy. The very thought of insurance might bring back memories of pushy salespeople, hard-selling tactics, and relentless nudges from that persistent relative or friend, all trying to get you to sign up for a policy. Why does this happen? The answer is straightforward – insurance needs to be “sold.” Most people don’t grasp the significance of insurance and won’t seek it out on their own.

This lack of awareness, combined with aggressive selling techniques by insurance companies, has tarnished the industry’s reputation and created a negative perception of insurance. In this blog post, we aim to bridge this knowledge gap and explain why life insurance is the most crucial financial product you’ll ever purchase.

What is Life Insurance?

Life insurance is a contract between you and an insurance company. You pay regular premiums, and in return, the insurer provides a lump-sum payment, known as a death benefit, to your beneficiaries upon your death. It’s a financial safety net designed to support those who depend on you.

Why Is Life Coverage Important?

Consider the story of Anil and Maya, a young couple in their early thirties with a bright future ahead. Both were working professionals, eagerly planning their future together. Anil, a software engineer, had just received a promotion, and Maya, a marketing executive, was pursuing further studies to enhance her career. They were thrilled about their plans to buy a new home and start a family.

Tragically, Anil was diagnosed with a terminal illness. Within a year, he passed away, leaving Maya devastated. Apart from dealing with the emotional turmoil, Maya was suddenly faced with the overwhelming financial responsibilities that Anil had shouldered. The medical bills had already drained a significant portion of their savings, and now Maya had to handle the mortgage on their new home, car loans, and her education expenses all by herself. Without Anil’s income, Maya found it extremely challenging to make ends meet.

If Anil had a life insurance policy, the payout would have provided Maya with the financial support she needed during this difficult time. It would have helped cover the medical bills, mortgage payments, and other expenses, allowing Maya to focus on her studies and career without the constant stress of financial insecurity.

This example illustrates the importance of life insurance, especially for single-income families or those with significant financial commitments. Life coverage helps prepare for unforeseen events, mitigating the financial impact of losing a loved one. It ensures that your family can maintain their quality of life and achieve their financial goals even in your absence.

The Financial Needs Hierarchy Pyramid highlights the essential role of life insurance in comprehensive financial planning. Building a solid foundation with appropriate insurance coverage is crucial before advancing to wealth growth and legacy building. Regardless of how much you save and invest, without managing financial risks through insurance, your financial stability can be as fragile as a house of cards.

How Life Insurance Works

Death Benefit

The amount paid to your beneficiaries upon your death, like the safety net under a high-wire act. This ensures your loved ones are financially secure even in your absence.

Premiums

Regular payments made to keep the policy active, similar to paying your phone bill to keep the service running. These payments can be made monthly, quarterly, or annually, depending on the policy terms.

Cash Value

A savings component in permanent life insurance that grows over time and can be accessed during your lifetime, like a savings account that earns interest. This feature provides financial flexibility for emergencies or other financial needs.

Types of Life Insurance

Life insurance can be broadly categorized into two main types: term and permanent insurance.

1. Term Life Insurance

- Level Term: Provides coverage for a specific period (e.g., 10, 20, 30 years) with a fixed premium. It’s like renting a house—you have coverage for a set time, but it doesn’t build equity, as insurance is not considered an investment product instead it has a saving component.

- Decreasing Term: The coverage amount decreases over time, typically aligned with a mortgage or other loans. Think of it as a shrinking umbrella that still keeps you dry during the critical years.

2. Permanent Life Insurance

- Whole Life: Whole Life insurance provides lifelong coverage with fixed premiums and includes a savings component known as the cash value. This cash value accumulates over time, offering a financial cushion that can be accessed if needed. While it’s not primarily an investment, the cash value component can provide added financial security alongside the death benefit.

- Universal Life: Provides flexibility in premium payments and death benefits, with a cash value that earns interest. Imagine having a flexible budget that adapts to your needs.

Variable Life Insurance and Unit Linked Insurance Plans (ULIPs) are similar but not identical. Both include investment options, allowing the policyholder to allocate part of their premium to different investment funds. Here’s a brief comparison:

3. Variable Life Insurance

Investment Options: Offers a range of investment options for the cash value, which can increase or decrease based on market performance.

Risk and Return: Similar to investing in stocks, there is potential for growth but also a risk of loss.

Flexibility: Policyholders can choose where to allocate their investments, but this requires regular monitoring and adjustments.

4. Unit Linked Insurance Plan (ULIP)

Investment Options: Part of the premium is invested in a variety of funds chosen by the policyholder (equity, debt, or hybrid funds).

Risk and Return: The returns depend on the market performance of the chosen funds. There is potential for higher returns but also a risk of losses.

Flexibility: ULIPs offer more flexibility in switching between different funds based on market conditions and investment goals.

In summary, both Variable Life Insurance and ULIPs provide a combination of insurance and investment, but they differ in structure, regulation, and the specifics of how investments are managed and accessed.

Who Needs Life Insurance?

- Parents: To ensure children’s future expenses are covered.

- Homeowners: To cover mortgage payments and prevent foreclosure.

- Business Owners: To protect business interests and ensure continuity.

- Anyone with Dependents: To provide for those who rely on your income.

- Individuals with Liabilities: To ensure debts and liabilities are paid off, preventing the financial burden from falling on surviving family members.

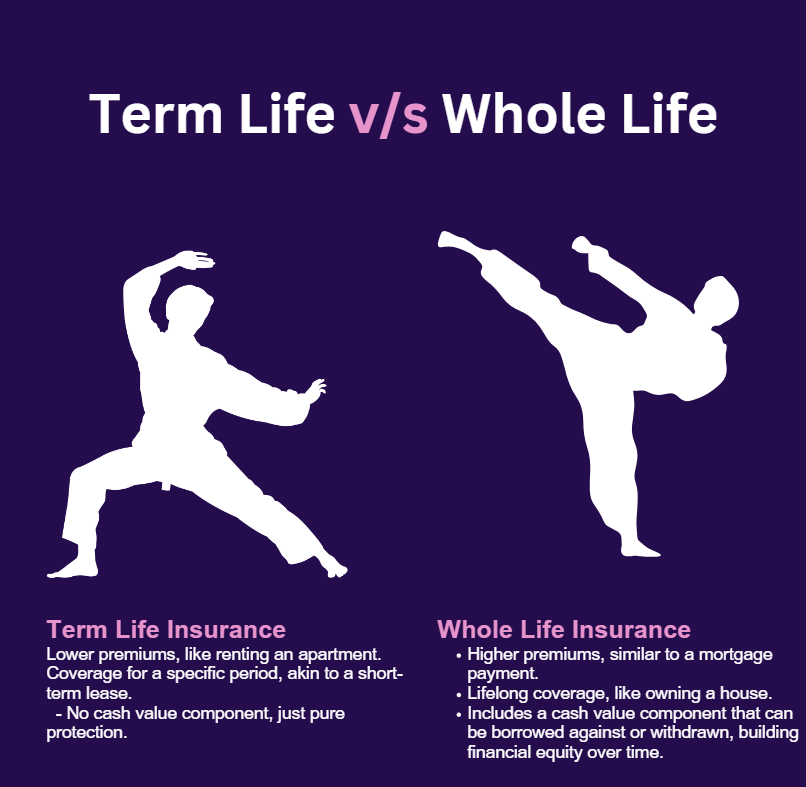

Term vs. Whole Life Insurance

Term Life Insurance

- Lower premiums, like renting an apartment.

- Coverage for a specific period, akin to a short-term lease.

- No cash value component, just pure protection.

Whole Life Insurance

- Higher premiums, similar to a mortgage payment.

- Lifelong coverage, like owning a house.

- Includes a cash value component that can be borrowed against or withdrawn, building financial equity over time.

Factors Affecting Life Insurance Premiums

Several factors influence the cost of life insurance premiums:

- Age: Younger individuals typically pay lower premiums, just as newer cars often have lower insurance costs.

- Health: Medical history and current health status impact premiums, like a clean driving record affects auto insurance rates.

- Lifestyle: Smokers and individuals with high-risk hobbies may pay more, similar to how risky drivers pay higher car insurance rates.

- Policy Type: Term policies are generally less expensive than permanent ones, like choosing between economy and luxury cars.

Life Insurance Buying Guide

1. Assess Your Needs

Determine how much coverage you need based on your financial obligations and goals. Consider factors such as your debts, future education costs for your children, and daily living expenses. This step is crucial to ensure that your loved ones are financially secure in your absence.

2. Research and Compare

Look at different policies and compare quotes from various insurers, much like shopping for a new gadget. Pay attention to the coverage, premiums, and benefits offered by each policy to find the one that best fits your needs and budget.

3. Check the Insurer’s Reputation

Ensure the company is financially stable and has a good track record, just as you would check reviews before buying a major appliance. Look for customer reviews, financial ratings, and the insurer’s history to make an informed decision.

4. Read the Fine Print

Understand the terms and conditions of the policy, including exclusions and riders, much like understanding a rental agreement. Make sure you know what is covered, what is not, and any additional features that might be beneficial.

How Cashvisory Can Help

At Cashvisory, we understand that navigating the world of life insurance can be overwhelming. Our team of experts is here to simplify the process for you. Here’s how we can assist:

- Personalized Assessment: We help you evaluate your financial needs and goals to determine the right amount of coverage.

- Comprehensive Comparison: We only focus on products that suit our users best. Our preference is to keep coverage and investments separate, and we can guide you on each aspect.

- Trusted Insights: Our insurance partner offer insights into the reputations and financial stability of insurance companies, guiding you to make a secure choice.

- Clarity and Transparency: We help you understand the fine print, including all terms, conditions, exclusions, and riders, so you are fully informed about your policy.

Choosing the right life insurance policy is a critical step in securing your financial future. Let Cashvisory be your guide in making this important decision with confidence and ease.

Benefits of Life Insurance

Financial Protection

Life insurance provides a crucial safety net for your family, ensuring they can maintain their lifestyle and meet financial obligations such as mortgage payments, education costs, and daily living expenses, even in your absence.

Tax Benefits

In the old tax regime, life insurance policies offer several tax advantages, including:

Tax-Free Death Benefits:** The death benefit paid to beneficiaries is generally tax-free, providing a substantial financial boost without the burden of taxes.

Tax Deductions on Premiums:** Under Section 80C of the Income Tax Act, premiums paid for life insurance policies are eligible for tax deductions up to ₹1.5 lakh per year. This benefit is available for policies on the life of the individual, their spouse, or children.

Tax-Free Maturity Benefits:** The maturity proceeds of life insurance policies are tax-exempt under Section 10(10D) of the Income Tax Act, provided certain conditions are met, such as the sum assured being at least ten times the annual premium.

Peace of Mind

Knowing that your loved ones are financially secure brings peace of mind, similar to having a robust emergency fund. This assurance allows you to focus on living your life without constant worry about your family’s financial future.

Additional Benefits in the Old Tax Regime

Critical Illness Rider: Premiums paid towards critical illness riders can also be claimed for tax deductions under Section 80D, providing additional financial relief if the insured is diagnosed with a critical illness.

By leveraging these benefits, life insurance not only provides financial protection but also serves as a valuable tool in comprehensive financial planning. At Cashvisory, we help you navigate these benefits to maximize your financial security and tax savings.

Before Getting Life Insurance

- Evaluate Your Financial Situation: Understand your current and future financial obligations, like assessing your monthly budget.

- Consult a Financial Advisor: Get professional advice tailored to your needs, just as you would consult a doctor for health issues.

- Review and Update Regularly: Ensure your policy keeps up with life changes like marriage, children, and home purchases, similar to updating your will.

When Should I Get Life Coverage?

Cost of Insurance

The best time to buy life coverage is as soon as you can. Getting term insurance earlier in life saves a lot of money in the long term. For example, a term plan purchased in your 20s costs a fraction of what it would in your 40s. The difference can be as significant as 300%.

Health

It is important to purchase life coverage when you are still healthy. If you delay the purchase, it might cost more due to health conditions. In fact, certain health conditions can make you uninsurable, meaning you might not be able to get coverage at all.

By understanding how life insurance works and the importance of securing it early, you can make informed decisions to protect your financial future. At Cashvisory, we help you navigate the complexities of life insurance, ensuring you choose the right policy at the right time.

Conclusion

Life insurance is more than just a financial product; it’s a commitment to securing the future of those you care about. By incorporating life insurance into your financial strategy, you ensure that your loved ones are protected no matter what life brings.